Term insurance plans are the most basic and cost-effective plans for individuals. They are designed to safeguard you and your family against mishaps and unforeseen circumstances by providing them with financial security.

Term insurance generally provides financial benefits in case the insured person dies. The plan is applicable during a specific period, also called the plan term. If the insured individual dies within this time period, the sum assured with the policy is paid to the nominees. The sum assured, along with the premium amounts, is chosen at the time of buying the policy. The benefits of this plan are generally applicable in case of the death of the insured. The plan hits maturity after completing the term period, and if the insured person is still alive.

Here, we will look at the different types of term life insurance plans that are available for purchase.

Level Term Plans

Level term plans are one of simplest term plans out there. For people who purchase this term policy, the sum assured remains constant during the tenure, and the benefit sum is only paid out to the nominee after the death of the individual.

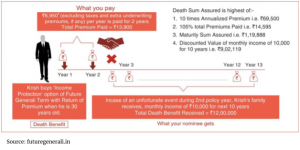

Return of Premium Plans

Unlike the traditional level term plans, the return of premium plans come with benefits after maturity, which means that the premiums are paid back to the policyholder if they survive the maturity period.

Increasing term plans

This term policy offers policyholders the choice to increase their assured sum annually while keeping the premiums the same. Due to this added benefit, these policies have higher premiums compared to level term plans.

Decreasing term plans

Much contrary to the increasing term plans, this plan keeps on decreasing with every passing year in order to meet the receding insurance requirements of the person who is assured. This policy is quite handy when the insured person has to pay EMIs as the assured sum keeps on decreasing at a chose frequency.

Convertible term plans

As the name suggests, these term plans can be converted to different plans at future dates. For example, suppose you have purchased a term plan which is to last you 20 years, but you do not want to carry on with the term plan and instead want to have it converted into a whole life insurance plan or an endowment plan. A convertible term insurance planning will allow you to do so without any hassle.

Term plans with riders

One of the other types of term life insurance is the one that comes with riders and added benefits — more than just providing the assured sum after the death of the insured. It comes with ride options such as critical illness cover, accidental death cover, and more. The insured can purchase these riders by paying a small premium amount alongside the normal term plan.

It is essential to pick the right kind of term plan to get the best benefits. Make sure that you, as a nominee, are informed about the benefits of these policies and the premiums that are to be paid for them, and then depending upon your needs and the risks you want to be covered, you could choose the ideal plan for you. You could also choose the return of premium plan if you want some sort of financial security after the policy reaches maturity.

Conclusion

Term insurance plans come with tax benefits: you can claim the premium paid for term life insurance plan as a deduction from your gross- total income in the financial year under section 80C. The death benefit payable as a lump sum is also tax-exempt under section 10(10D) for your dependents.

Another benefit of a term policy is that it comes with a lot of flexibility and regular income benefits. You have the option to select from plans that will offer regular income benefit to your dependents. You also get to choose between plans that return all premiums paid for the cover if you survive the tenure of the cover.

Term insurance for life can come to your aid and can provide numerous benefits if you have family members who are wholly dependent on you — if you are the only bread earner of the family. Various types of term life insurance can also come to handy if you have certain liabilities to pay off, such as a home loan or a car loan.

{kind=link}